Going from a niche product to mainstream adoption, Bitcoin has surpassed Internet giants like Facebook in market capitalization after more than a decade of development. While it has not become the "peer-to-peer payment system" envisioned by Satoshi Nakamoto, it went further and further down the road of being a repository of value, being added to the balance sheets of an increasing number of companies, and is moving in the direction of becoming a "super sovereign currency".

Due to the lack of programmability in the Bitcoin network, Bitcoin, the oldest and most well-known cryptocurrency, has limited applications in its own network. The emergence of BTC-pegged tokens has created a broader stage for Bitcoin to expand into Turing-complete blockchains such as Ethereum and participate in a thriving DeFi ecosystem as the most popular underlying asset.

The Bitcoin network is still the most secure blockchain network

The Bitcoin network was the first blockchain to emerge, and it remains the most secure and well-known cryptocurrency today, as seen by on-chain data. According to Glassnode, as of July 18, there were about 640,000 active Bitcoin addresses, with 9 million addresses holding greater than 0.01 BTC, and 1.17 million BTC transferred on-chain each day, which equals about $36.9 billion, equivalent to Bolivia's annual GDP, and only 94 countries had a GDP exceeding that value in 2020.

Each new bull market in Bitcoin is accompanied by an influx of more users, and it is arguably the growing number of users that has caused the price of Bitcoin to rise, with the current bull market being driven by the adoption of Bitcoin by large institutions. In October 2020, international payments giant, PayPal, announced its entry into the cryptocurrency market, allowing users to use PayPal's online wallet to buy, sell and hold Bitcoin and other cryptocurrencies. Almost at the same time, Singapore's DBS Bank announced the launch of a digital asset trading platform with support for trading cryptocurrencies such as BTC. Since then, companies such as Tesla and Meitu have started buying Bitcoin. Bitcoin is gradually moving from niche to mainstream adoption.

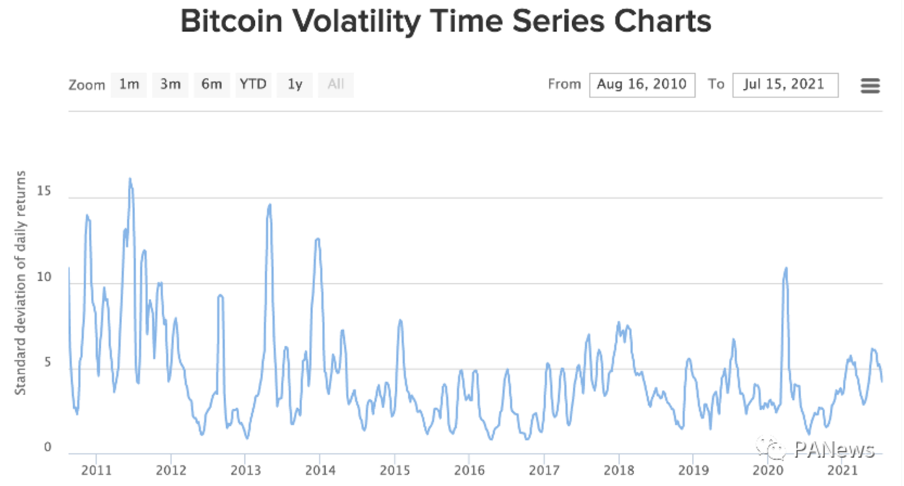

Bitcoin's huge volatility is overwhelming for many investors, but it is becoming less volatile as more powerful institutional buyers gradually work their way in. According to BitPremier statistics, Bitcoin's 30-day volatility has been trending downward overall from 2010 until now. Even during last year's 3.12 period, volatility was not as high as it was during 2010-2014. The lower volatility has also allowed Bitcoin to be offered by institutions as an alternative asset class. Because there is no correlation between Bitcoin and most mainstream assets, holding a portion of Bitcoin can enhance the diversity of an institution's basket of assets.

Throughout its history, after numerous crises, Bitcoin has gained popularity and a stronger global consensus. On August 1, 2017, some miners executed a hard fork at Bitcoin block height 478558, and then BCH was born. After that, BCH was forked again to BSV, and both have called themselves "the real Bitcoin". But the price ratio to Bitcoin kept going down. In 2014, MtGox, once the largest cryptocurrency exchange in history, collapsed due to the theft of $400 million worth of cryptocurrency. On September 4, 2017, Chinese exchanges began going offshore due to increasing regulations.

"What doesn't kill you, makes you stronger." Although increasing regulations and hacking incidents have never stopped, Bitcoin still managed to become the safest blockchain network. Altcoins (Bitcoin alternatives), on the other hand, are more susceptible to security issues. An example is the double-spending attack on Bitcoin BTG in 2018, which resulted in a 110 million financial loss in RMB to the exchange and now leaves the BTG price at less than 10% of its 2017 high.

The value of BTC's premium assets should have more applications

BTC, as the highest quality crypto asset, should be widely used, but the lack of programmability, long block-out time, and limited block capacity of the Bitcoin network itself has limited the daily use of BTC, and expansion solutions such as the Lightning Network, which was once seen as a great hope, have also developed slowly. With the prosperity of the Ethereum ecosystem, BTC has begun to be widely used as an underlying asset in DeFi applications on Ethereum. Currently, more than 1% of all Bitcoin-pegged tokens have been issued on Ethereum, and this number continues to grow.

Introducing BTC as a cross-chain asset to other blockchains can benefit other public chains, coin-holding users, and the Bitcoin network itself.

Benefits to other public chains

Bitcoin's high market cap, high liquidity, and low volatility is a premium asset for any public chain, hence the widespread use of Bitcoin-pegged tokens as an underlying asset in lending protocols on Ethereum. The introduction of Bitcoin is even more important for other public chains that lack such kinds of assets.

The increase in asset types also makes the DeFi Lego stack more secure. Before last year's 3.12, assets on Ethereum were relatively homogeneous, leading to a large number of assets being liquidated when the market fluctuated. In MakerDAO, a massive number of users needed DAI to repay their loans, and the premium for DAI rose to over 20% at one point. If DAI could be borrowed by pledging a wider variety of assets, it would decrease the fragility of the lending protocol, a problem that has been solved with the use of cross-chain Bitcoins such as WBTC.

Benefits for Bitcoin Holders

For Bitcoin holders, using Bitcoin on other chains by way of cross-chaining can effectively reduce costs and increase usage scenarios. There are multiple advantages to using Bitcoin-pegged tokens:

- The transaction cost is lower. With no network congestion, the average transaction cost on the Bitcoin network is about $5. With a Gas Price of 10 GWEI on the Ethereum network, the cost of an ERC20 token transaction is about $1. The cost on other chains such as Solana, Polygon, Harmony, etc. is even lower, basically negligible.

- Transaction confirmations are faster. Bitcoin's block-out time is about ten minutes, and Ethereum's about thirteen seconds, while new emerging public chains can complete the transaction in a few seconds.

- Serves as a premium asset in decentralized lending, trading, derivatives, bonds, and other DeFi protocols, such as the ability to borrow stablecoins and other assets by pledging Bitcoin-pegged tokens.

- Helps cryptocurrency-holding users gain revenue, which is not possible in the Bitcoin network.

Benefits to the Bitcoin Network Itself

For the Bitcoin network itself, cross-chain Bitcoin can also increase Bitcoin's consensus.

- Cross-chaining means that Bitcoin can be accepted by more users on other networks, thus increasing the number of users holding BTC in an alternative way. According to data on the Ethereum blockchain browser, the number of addresses that hold WBTC has increased to 33,046.

- It is beneficial to consolidate Bitcoin's position as a repository of value. Native Bitcoins are pledged in the Bitcoin network, which does not affect Bitcoin's role as a value store. And the yields gained from other networks can be converted into more Bitcoin assets.

- It is conducive to increasing the actual utility of Bitcoin. Bitcoin's slow block-out speed makes it difficult for a variety of applications to be deployed, as transactions can take up to 10 minutes to upload on-chain and about an hour to wait for 6 block confirmations. The practical use of Bitcoin is better served by the form of BTC-pegged tokens, and blockchains such as Ethereum have much faster transaction confirmations, allowing for 10 block confirmations in three minutes.

BTC-pegged tokens Issuance Methods

Bitcoin-pegged tokens are a class of tokens that are issued on non-Bitcoin networks and whose price is pegged to the native Bitcoin. Currently, the most frequently used Bitcoin-pegged tokens include WBTC, HBTC, renBTC, sBTC, oBTC, and pBTC. As of July 19, 262,642 Bitcoin-pegged tokens have been issued on Ethereum alone, and they are issued in different ways.

Cross-chain VS Synthetics

Bitcoin-pegged tokens can be divided into two implementations, cross-chain and synthetic, based on the underlying assets locked in.

Cross-chain

Bitcoin-pegged tokens implemented in this way have their native Bitcoins locked 1:1 in the Bitcoin network, and then the pegged tokens are minted on other blockchains. Several of the most widely used Bitcoin-pegged tokens are currently implemented in this way, such as WBTC, HBTC, and renBTC.

Synthetics

Bitcoin-pegged tokens generated in this way do not have real BTC as collateral but are "simulated" by pledging other tokens to mint an asset equivalent to the value of Bitcoin, such as sBTC and xBTC.

Comparison between the two: Bitcoin-pegged tokens that are implemented by cross-chaining have real Bitcoins as collateral in the Bitcoin network, and this process does not generate additional Bitcoins, only mapping Bitcoin assets 1:1 to other chains. Bitcoins generated through synthetics, on the other hand, do not have native Bitcoins underpinning them and have to rely on Altcoins, which are much less liquid and more volatile, to be pledged as collaterals, resulting in both low capital utilization rates and insufficient security. From this perspective, it makes more sense to build BTC-pegged tokens in the cross-chaining way.

Centralization VS Decentralization

One problem with issuing Bitcoins across chains is the custody of the underlying assets. Users' native Bitcoins need to be pledged 1:1 to the Bitcoin network, and these Bitcoins need to be held by someone who issues "proof" of receipt to the user, often referred to as the "custodian". There are two types of custodians that hold assets: centralized and decentralized.

Centralized

In a centralized issuance of Bitcoin-pegged tokens, the custody is done by a single entity, such as BitGo, which holds all the collateral needed to issue WBTC. According to Wikipedia, BitGo was founded in 2013 by Mike Belshe and Ben Davenport and is a digital asset trust and security company based in California, USA. (https://en.wikipedia.org/wiki/BitGo)

Decentralized

Instead of being controlled by a single entity, custody is held by a decentralized network. In renBTC, for example, users’ native Bitcoins are hosted by Ren Virtual Machines (RenVMs), also known as dark nodes. tBTC ensures decentralized custody with a system that randomly selects the signatories (known as signers) that create and manage the BTC wallets.

Comparison between the two: A centralized custodian is more likely to have a single point of failure, such as loss of assets or even active theft by the “custodians”. A decentralized custodian approach is the current trend and is more in line with the spirit of the blockchain.

Minting Cap & Liquidation Risk

In decentralized Bitcoin-pegged tokens offerings, in order to maintain the security of the underlying assets and prevent the custodian from committing theft, in addition to the user needing to pledge native Bitcoin 1:1, the custodian also needs to pledge assets in order to do their job. The custodian usually pledges not Bitcoin but another altcoin, and thus may need to overcollateralize to ensure safety.

In existing schemes, renBTC chooses to use REN tokens as collateral for its nodes, where dark nodes need to register and pledge 100,000 REN tokens as collateral. tBTC uses ETH as collateral and pledges no less than 1.5 times the assets under custody. In Synthetix, the overall pledge rate of synthetic assets is even higher than 588%, which means the number of BTC-pegged tokens generated is limited by the collateral, while the over-collateralization can also cause a great waste of funds.

According to data from CoinMarketCap on July 15, the current market cap of REN is $326 million, and renBTC's market cap has surpassed that of REN. Ren's official documentation shows that the ideal pledge rate for renBTC is above 300%, and as long as it is not less than 100%, the assets are safe, but now that renBTC's pledge rate is less than 100%, RenBTC's issuance may be nearing its upper limit and cause a security risk.

As demand for Bitcoin-pegged tokens increases, the mint cap will become more and more of a problem, and there are already multiple protocols looking to reduce collateralization rates and increase efficiency in the use of funds. For example, Synthetix passed a proposal in August 2020 to lower the collateralization rate from 700% to 600%, and oBTC recently sought to lower the collateralization rate from 125% to 115%, with the vote having been held on SnapShot and gathering 94.17% of support.

The current custodian approach also faces another problem, with meme coins pledged by the “custodians” that are much more volatile and may not be able to be relied upon to maintain the security of the network when their prices fall significantly in the short term, and custodians may join forces to steal native Bitcoins pledged by users.

Ideal Properties of Bitcoin-Pegged Tokens

As mentioned above, the ideal Bitcoin-pegged tokens should have native Bitcoin as collateral for minting users, be issued in a decentralized form, have sufficiently high capital utilization and minting caps, and have sufficiently low liquidation risk. According to PANews, the ideal properties of Bitcoin-pegged tokens would need to include:

- Fairness: A fully decentralized asset custody, with equal weights between custodians who are randomly selected and permission-less to join and leave the custodian network at will, thus preventing a single point of failure of a custodian, making it impossible for one custodian to steal the native BTC assets in the system.

- Security: The minting user's collateral is native Bitcoin, and the mapping is done 1:1 in a new network, with no risk of ever decoupling.

- Audit-less: No KYC. Anyone can create, exchange and use Bitcoin-pegged tokens, regardless of their identity or what jurisdiction they are in.

- High minting capacity: There should be no upper limit to the number of Bitcoin-pegged tokens that can be minted due to the design of its own mechanism, which means the number of Bitcoin-pegged tokens that can be minted should be guaranteed to be as large as possible.

- High capital utilization: The collateralization rate of the custodian should be as low as possible with sufficient network security, and the price of the collateralized assets should be stable enough to increase capital utilization. Most BTC-pegged tokens in the market have a total pledge rate of 250% or more (sBTC: 600%, tBTC: 250%). The higher the total pledge rate, the less efficient the funds are.

To solve the above problems, DeCus proposes a new decentralized cross-chain minting scheme.

First of all, the collateral of the custodian is BTC assets, initially WBTC, and then gradually extended to other cross-chain BTCs, including the cross-chain BTC minted by itself. Theoretically, the system of DeCus can accommodate all types of Bitcoins to be used as custodian’s collateral.

According to an SCI paper by Dr. Guang Yang, the research director of Conflux, DeCus brings an efficient custodian model with a self-regulating custodian network that can allow custodians to carry out secure and stable custody without over-collateralization.

According to DeCus' overlapping grouping scheme, as the network matures with more custodians joining in the network, the collateral rate will subsequently decrease.

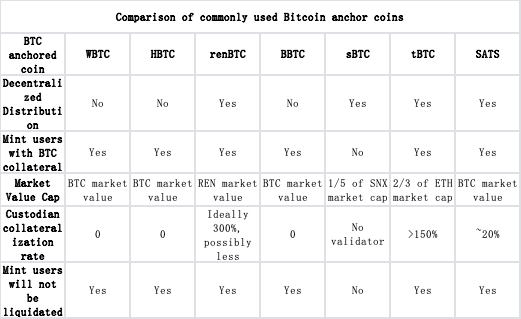

According to the table above, DeCus has three core advantages, namely, complete decentralization, low collateralization rate for custodians (about 20%) along with high capital utilization, and no liquidation and decoupling risks as both users and custodians pledge Bitcoins. Likewise, DeCus' cross-chain BTC maintains the advantages brought by other blockchains such as faster transaction confirmations and cheaper transaction fees.

In addition, DeCus plans to split cross-chain BTC to make it easier to use. 1 BTC is worth too much today, so DeCus will issue a split coin of Bitcoin, SATS, where 1 BTC = 100 million SATS, with the ability to swap between SATS and BTC at any time at a fixed ratio. Because of the native BTC pledged by mint users and the cross-chain BTC pledged by the custodian, SATS will be safe enough.