Bitcoin is back.

October was nothing short of amazing for bitcoin with big headlines and big price gains. Here's a quick recap of what bitcoin has done so far.

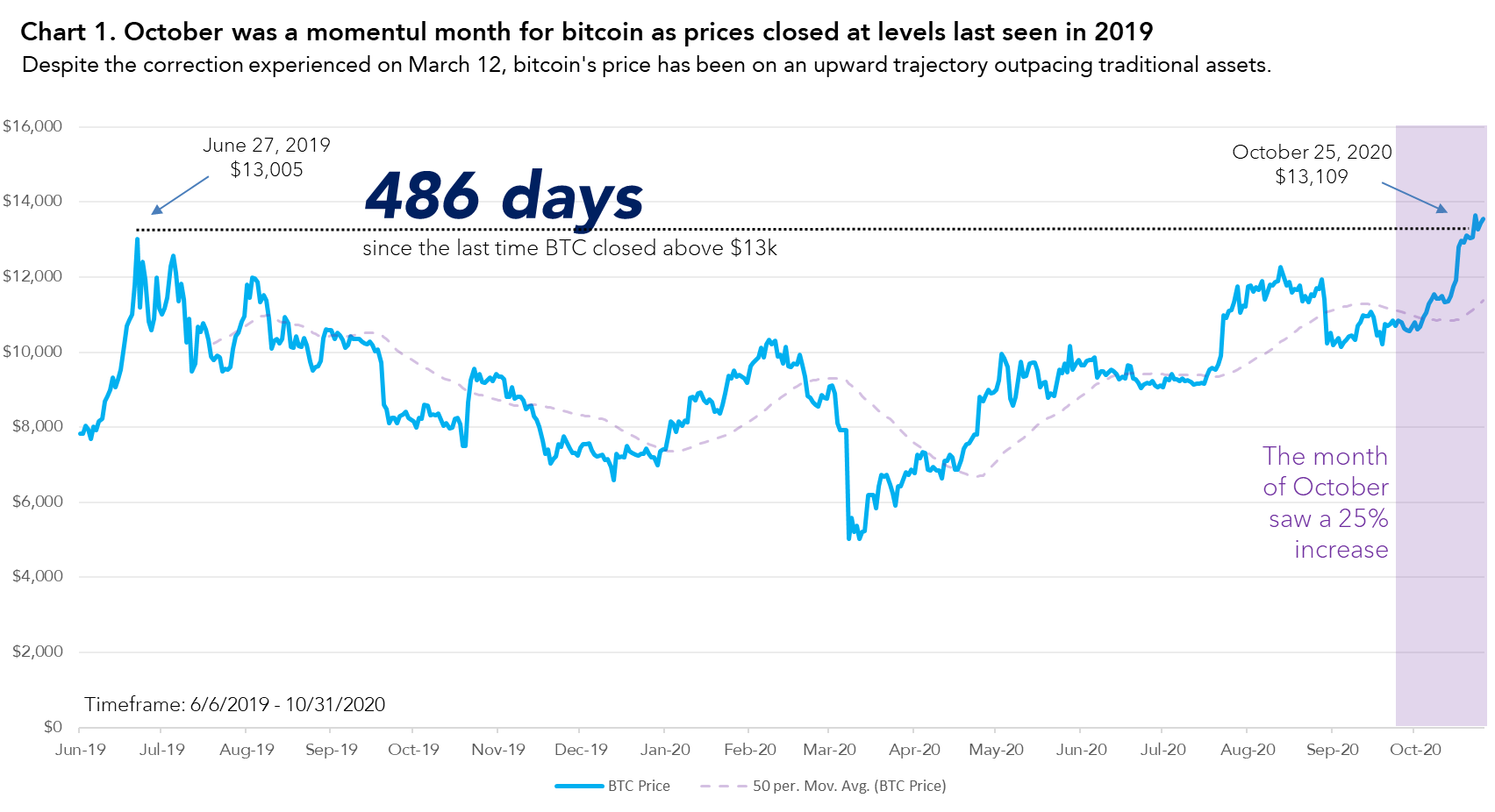

Price movement for bitcoin can be symmetrically mirrored more or less exactly near the March drop as this would form a V shaped line. Near the end of October, BTC has reached back to price levels not seen back in June of 2019 with closing prices above the $13k level. This is in part thanks to the 25% increase of BTC in October due to the monstrosity of blockbuster headlines of institutions FOMO’ing into bitcoin. It started this summer with Microstrategy, then Square, then Paypal, then DBS, and a host of other public companies announcing their beliefs in the digital gold asset. We expect to see more rushing in as the third bull wave is highly anticipated throughout the year of 2021.

It took 486 days and a heavy correction felt on March 12, but prices are finally back to levels where optimism for ATHs are being called for.

In traditional markets, the S&P 500 index and Gold have both dropped 3.2% and 1.1%, respectively. Investors and the economy is surely embracing for election results at the time of this writing (November 4th 11:24 UTC+8) which would give a big shakeup for the month of November. Whether or not the US gets a blue or red win, bitcoin will surely be on a tear of its own.

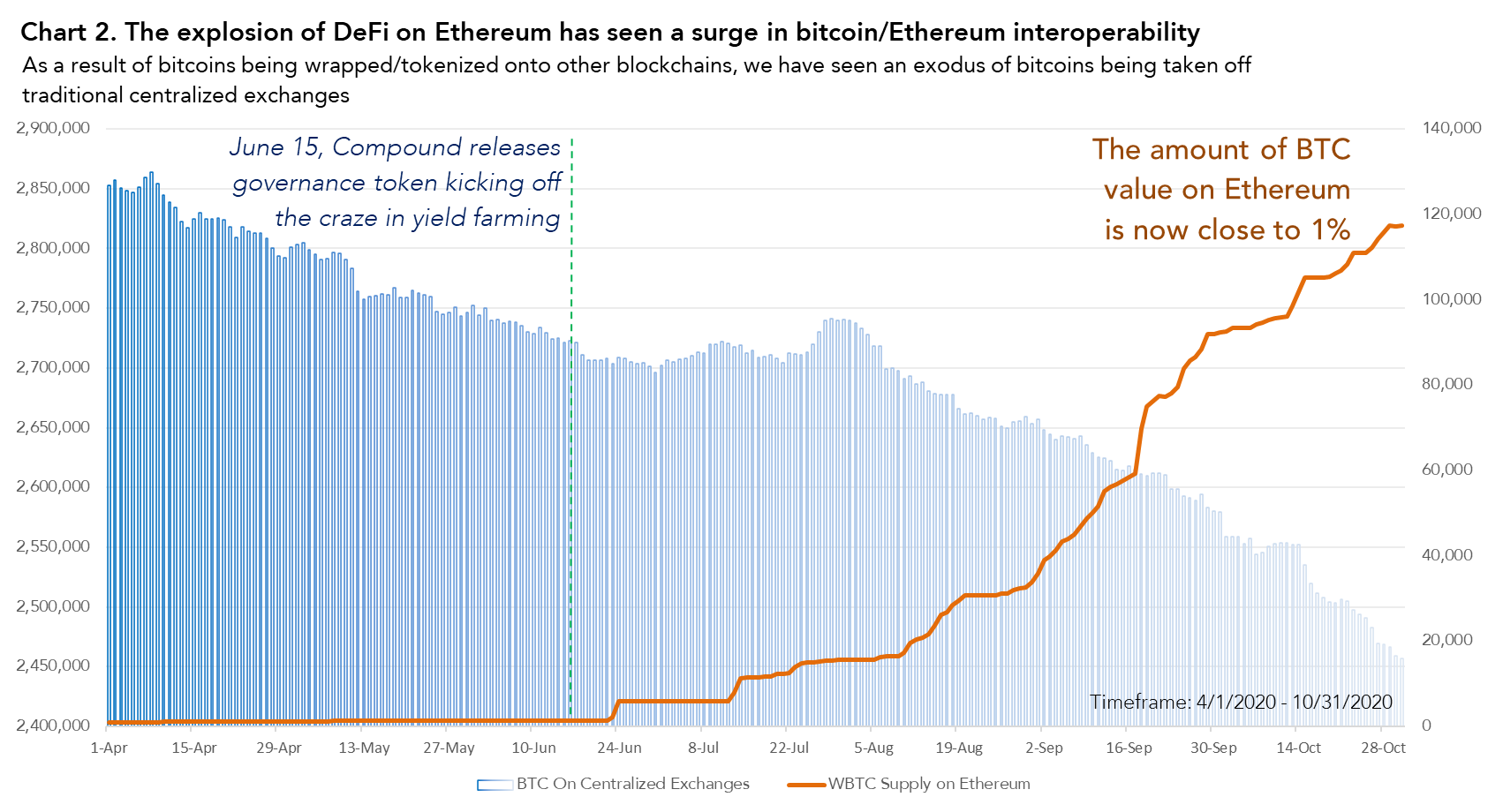

There has been an inverse relationship for the past few

months between the amount of WBTC supplied and the amount of bitcoins on

exchanges. Although not proved to be correlated or having a causation

relationship, the pattern is apparent. On April 1, the amount of bitcoins on

the major centralized exchanges, as calculated by Glassnode analytics, was

around 2,850,000. This number has dropped over 15% to around 2,450,000

bitcoins.

To give some clarity, the trend of wrapping, or tokenizing,

bitcoins has enabled bitcoin holders to use their bitcoin values on other

blockchains, specifically Ethereum, which has boasted the DeFi explosion we

have seen. This interoperability between blockchains can also be misconstrued

to believing bitcoin network activity will ultimately decrease because of the

former. Hard to prove but the hypothetical implications are worth noting. Or

the decrease in bitcoins on exchanges could be a realization of the proverbial

“not your keys, not your crypto”, which has been accentuated with the

controversy surrounding OKEx.

Postulating on how exactly is still a bit unclear, but the controversy surround the OKEx exchange has presumably in some way dropped their bitcoin mining pool out of the top 10 pools based on total hashrates. This subsequently has also seen the total amount of bitcoin hashrates decrease from 146 EH/s to currently 107 EH/s, which constitutes a near 30% drop. Other factors may have also contributed such as the annual transition of miners moving out of Sichuan to Xinjiang for lowered cost electricity or the upcoming controversial BCH fork.

The simultaneous drop in hashrates and increase in price have made this period a profitable one for bitcoin miners as difficulty of mining has subsequently been reduced by 15%. On the flipside, the reduction in miners and hashrates have also seen a backlog in the number of unconfirmed transactions in the mempool, which as a result, have pushed transaction fees to levels considered expensive for the Bitcoin network. This should eventually revert back to normal levels as the once idled miners come back online during this lucrative mining period.